Market Insights - July 2023

The Death of the Dollar?

Key Points:

Commentary around the decline of the United States as the planet’s sole hegemon has intensified in recent years in response to the growth of China’s economy and souring in tensions between China and the West.

In the West, a desire to shore up supply chains and re-shore manufacturing is the inevitable result of the tail risk that conflict breaks out between China and Taiwan.

Russia’s invasion of Ukraine and subsequent sanctions has intensified desires in the “non-West” to do the same, particularly with respect to currency reserves and payments systems.

All of the above is consistent with a trend towards multi-polarity in the global economic and political system. We think this trend will continue and intensify in the decades ahead.

Though the short-term consequences for investment markets are expected to be limited, there are longer term implications for investors.

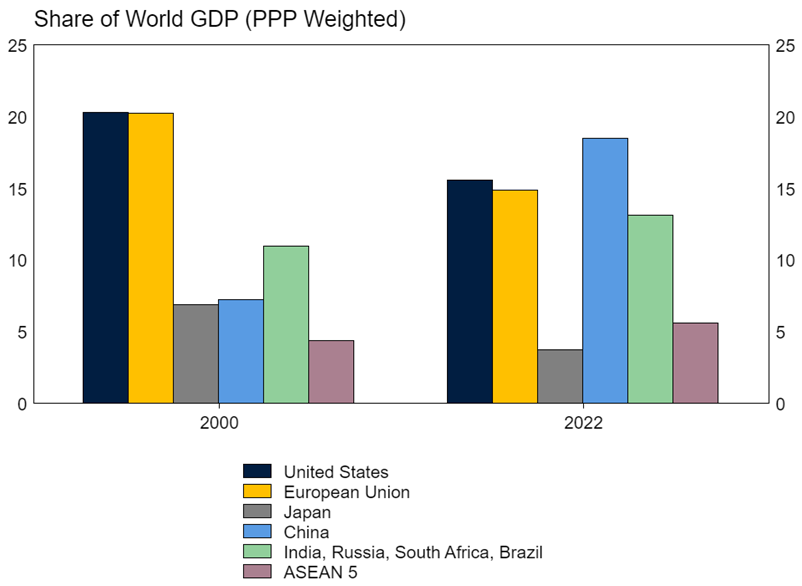

The US and Europe have shrunk as a share of global economic activity meaningfully in the past two decades, reflecting stronger growth in China and other emerging economies. On a PPP basis, China is now the largest economy in the world. On a nominal GDP basis, it is the world’s second largest economy. The size of the BRICS (Brazil, Russia, China, India and South Africa) economies ex China is similar to Europe and the United States.

As these economies have become larger, they have demanded a larger say in global political affairs, seeking to expand their spheres of influence and provide input into global political norms and rules. To date, the rise of these economies has been largely peaceful and orderly. Russia being a standout exception both in terms of peacefulness and expanding influence. Clearly, since the dissolution of the USSR, Russia’s influence and relative economic power has been in structural decline.

Over the past few decades, the optimist’s view of this peaceful rise is that as these countries became wealthier, they would fall into line under the existing global political order – one which is dominated by the ideals of western liberal democracy. The probability of this optimistic outcome has deteriorated substantially over the past decade. In practice, many of these growing economies are not liberal democracies and do not wish to operate under the currently established rules of the game. Even those who are democratic want to operate in their own national interest, which doesn’t always align with the interests of the United States, UK or Europe.

Hence, we have the emergence of a multipolar system, where we have major developing economies wishing to decouple from the West. There are three key investment implications of this:

Changes to the global trade system, which have implications for growth, inflation and currencies;

Heightened sovereign risk when investing offshore given the potential for rule changes; and

The risk of actual conflict, given that countries that trade together historically have been less likely to fight wars against each other.

De-Dollarisation

The US dollar is the world’s currency. It dominates global trade, foreign exchange reserves, derivative transactions, commodity pricing and the global payments system. None of this should be a surprise. The US was the world’s largest single currency economy by far during the development of the modern financial system.

Source: IMF

Source: Bank for International Settlements as at April 2022

Having most of the world’s inter-country economic activity priced in its own currency provides the United States with considerable leverage over other nations. The exclusion of Russia from much of the developed world financial system following its invasion of Ukraine is a key example of this. Naturally, countries who see themselves as potentially facing the ire of the United States at some point in the future would be interested in avoiding this leverage. The ideal way to do this would be to provide a credible alternative to the US Dollar.

This is incredibly difficult to do. Unseating the existing standard requires something better, and there is nothing close to better. Nor is there likely to be at any point in time. As Larry Summers quipped in 2020, "Europe is a museum, Japan is a nursing home, and China is a jail.”

While there may not be a credible alternative to the US Dollar, other currencies are gaining ground. The US Dollar’s share of foreign exchange reserves has fallen from around 70% to around 60% in the past two decades. However, most (around 75%) of the decline has been due to a rise in other developed market currencies, rather than a switch to CNY (around 25%). In practice, FX reserves need to be invested in markets by reserve managers and there is no market other than US Treasuries which is deep and liquid enough to house the roughly US$12 trillion in global reserves. Indeed, IMF analysis in 2022 came to the conclusion that the reduction in US Dollar reserves over the period reflected a desire for portfolio diversification by reserve managers.

Outside of FX reserves, there is more practical room for movement away from the US Dollar. In particular, in 2015 China launched CIPS, an alternative payment and clearing system to the US dominated SWIFT intended to support the internationalisation of China’s currency. Usage of the system picked up after the SWIFT ban against some Russian banks in 2022. While CIPS takes a very small share of payments versus SWIFT, it is likely that this share will continue to grow. A number of countries are settling bilateral commodities trades in their own currencies. BRICS members have discussed the development of an alternative currency and other developing countries have discussed joining the group. Some have flagged cryptocurrencies as a vehicle to unseat US Dollar dominance. While Bitcoin is too impractical to achieve this outcome, some central banks (including China’s) have introduced, or spoken about introducing central bank backed digital currencies. Potentially this addresses the issue of needing something “better” to unseat the US Dollar.

Even if there is a meaningful shift over time away from the US Dollar in payments, trade invoicing, FX transactions or FX reserves, the market impact will be relatively limited. The US Dollar would almost certainly weaken structurally versus other currencies, but the impact should be gradual. The bigger implications are driven by the factors causing any de-dollarisation in the first place, the emergence of a multipolar global system.

The most obvious implication is inefficiency. Global trade has been so successful at lifting poor countries out of poverty and making rich countries richer because people, corporations and countries who have a natural advantage in certain areas of production are able to produce at a global scale. The US builds the best tech companies. Taiwan makes most of the semi-conductors. London is the world’s currency trading hub. Australia digs up a lot of dirt. Particularly in areas of national strategic importance, decoupling means a focus on re-shoring previously foreign production and securing supply chains. We can see the impact of the passing of the CHIPS and Inflation Reduction Acts in the USA, which were designed to boost semi-conductor and green energy production in the charts below.

Impact of CHIPS Act and the IRA

While this makes supply chains and infrastructure more robust, it costs a lot of money to do. As a result, these activities generally increase debt and make things more expensive to produce (more inflation).

Heightened Sovereign Risk

The global financial system is governed by many, many rules. These rules ensure contracts are enforced, everyone is speaking the same language and generally protect investors against bad actors. A decoupling of global financial markets makes this system more complicated and increases the risk that investors will not be as protected as they anticipated.

As markets move away from one system of rules governing almost all activity to region or bloc specific rules, many of which will increasingly be geared toward the national interest, rather than foreign investor interest, investors should demand a higher sovereign risk premium for investing in these markets. To the extent that the rules of the game are in place to favour the national government / national champions (state owned enterprises in China for example), it may simply be a bad idea to invest in these economies.

Risk of Conflict

Countries who trade together tend not to fight each other. Decoupling reduces trade between countries and therefore increases the risk of conflict. Add to this a desire for countries and regions with growing political and economic power to shape the wider world in their own image, rather than in the image of the West, and the prospects for conflict rise further still.

The obvious political response to an increased risk of conflict is increased military spending. Many governments will need to replenish stockpiles worn down by support for Ukraine. European NATO participants are likely to increase their defence spending towards the 2% NATO pledge. Australia is about to spend an unfathomable amount of money on 11 new submarines (roughly the equivalent of a moderately priced hatchback for every Australian household, assuming the project comes in on budget). China is planning to increase the size of its navy from 340 vessels in 2022, to 400 in 2025 and 440 by 2030.

Defence spending is fiscal stimulus. In a world that may also be drowning in net zero spending the combined effect will likely be very inflationary. Many developed market economies are already on an unsustainable fiscal path due to ageing populations and the associated spending commitments. Spending upon spending and ever higher debt may finally force markets to question whether government bonds are still a safe asset.

The risk of conflict also directly influences portfolio allocations. As Australian domiciled investors, we need to be very careful holding assets in any jurisdiction we are at risk of going to war with.

Summary

The post-Cold War Pax Americana of the past few decades is likely to become increasingly fractured in the decades ahead. We think geopolitics will again become a source of market instability. We also think from a directional perspective, the outcome of a multipolar world is higher government spending, debt and overall inflation. Global economic growth will also likely suffer, as more economies are pulled away from Western capitalism and embrace increasingly illiberal models, benefiting national elites and vested interests at the cost of aggregate prosperity. Navigating the above will require more careful and considered portfolio management than was necessary in the previous few decades.